Short interest into FDA decisions

1. How shorted is biotech going into an FDA decision?

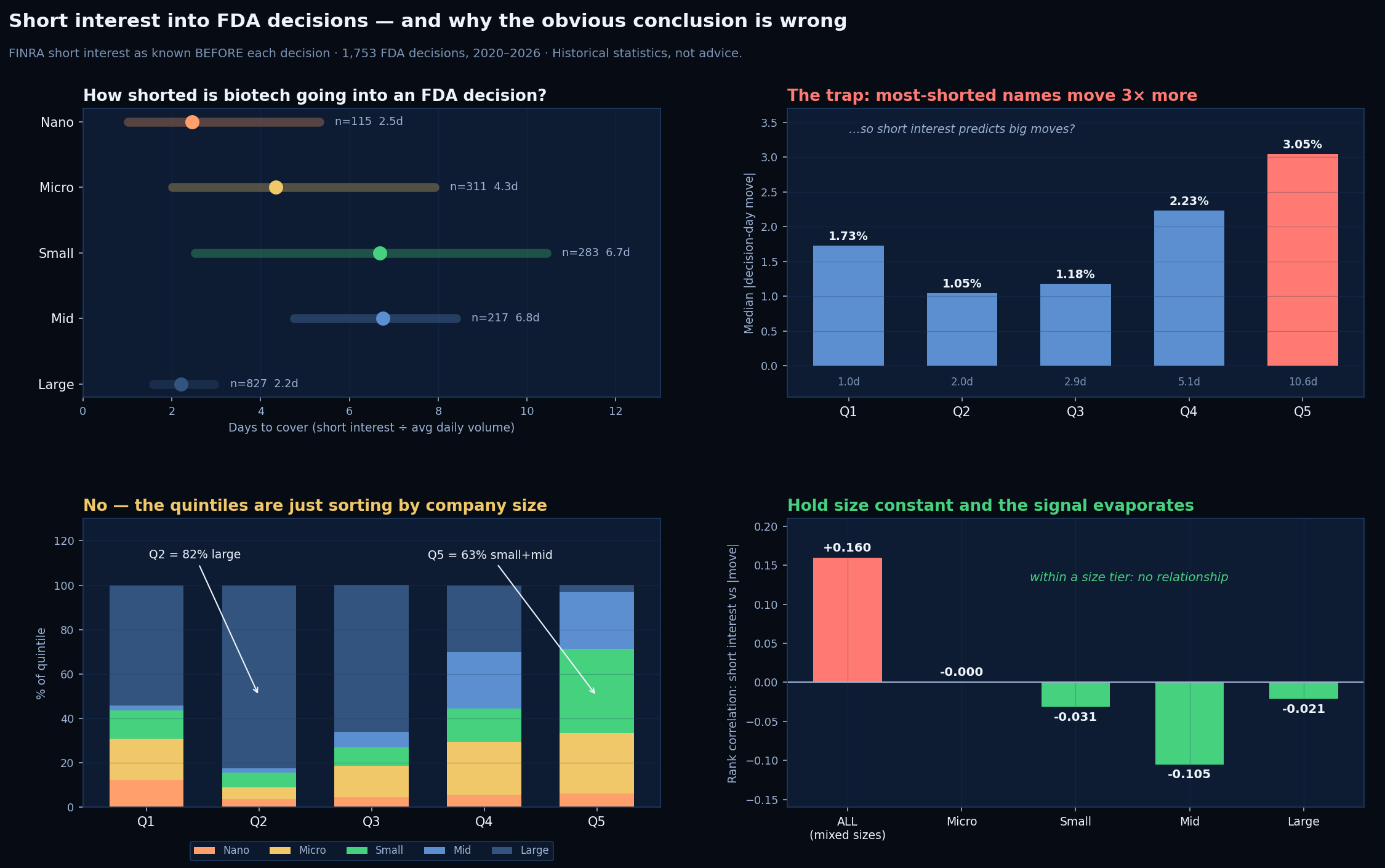

This is the part nobody publishes. Days to cover = short interest ÷ average daily volume: how many days of normal trading it would take shorts to buy back.

| Cap tier | n | Median days to cover | 25th pct | 75th pct |

|---|---|---|---|---|

| Nano | 115 | 2.5d | 1.0d | 5.3d |

| Micro | 311 | 4.3d | 2.0d | 7.9d |

| Small | 283 | 6.7d | 2.5d | 10.4d |

| Mid | 217 | 6.8d | 4.8d | 8.4d |

| Large | 827 | 2.2d | 1.6d | 3.0d |

Small- and mid-caps carry by far the heaviest short interest into an FDA decision (≈6.7 days) — roughly 3× a large-cap. Nano-caps are counter-intuitively low at 2.5 days: they are hard and expensive to borrow, so shorts often simply can’t build a position.

2. The trap

Now bucket every decision into five groups by short interest, and look at how big the decision-day move was:

| Quintile | n | Median days to cover | Median |move| | % large-cap | % small+mid |

|---|---|---|---|---|---|

| Q1 | 356 | 1.0d | 1.73% | 54% | 15% |

| Q2 | 346 | 2.0d | 1.05% | 82% | 9% |

| Q3 | 350 | 2.9d | 1.18% | 66% | 15% |

| Q4 | 350 | 5.1d | 2.23% | 30% | 40% |

| Q5 | 351 | 10.6d | 3.05% | 3% | 63% |

Q5 moves 3.05% versus 1.05% for Q2. Across all 1,753 events the rank correlation is +0.160. A tempting headline — “heavily shorted biotechs move 3× more into FDA decisions” — is sitting right there.

3. Why it’s wrong

Look at the last two columns of that table. The quintiles aren’t sorting by short interest — they’re sorting by size. Small- and mid-caps are both more shorted and naturally more volatile. So we ran the only test that matters: hold company size constant.

| Within cap tier | Correlation: short interest vs |move| |

|---|---|

| All events (mixed sizes) | +0.160 |

| Micro | -0.000 |

| Small | -0.031 |

| Mid | -0.105 |

| Large | -0.021 |

Inside a single size tier, short interest tells you nothing about how big the move will be — the correlation is zero, and if anything slightly negative. The apparent signal was a Simpson’s paradox: a real pattern in the pooled data that reverses or disappears once you condition on the confounder.

Method

Data. FINRA bi-monthly short-interest filings, matched to each FDA decision by ticker. Point-in-time. For every event we use only the short-interest reading already published before that decision (median lag 9 days, 95th percentile 15) — no lookahead. Measure. Days to cover = short interest ÷ average daily volume. Move. The absolute decision-day reaction; we deliberately do not report direction. Reporting which way heavily-shorted stocks went would be an approval-odds claim in disguise, and we don’t do those. Statistics. Median, interquartile range, and Spearman rank correlation. Rows with stale short interest (>45 days old) or implausible days-to-cover (>60) were excluded.

2. Days to cover embeds volume. It is a ratio, so a volume spike shrinks it without a single share being covered.

3. Absence of evidence. We found no within-tier relationship. That is not proof none exists — only that, at this sample size and with this measure, there isn’t one worth acting on.

“pdufa.bio, Short interest into FDA decisions (2020–2026), n=1,753, https://www.pdufa.bio/research/short-interest-fda”

Journalists & researchers: data@pdufa.bio.